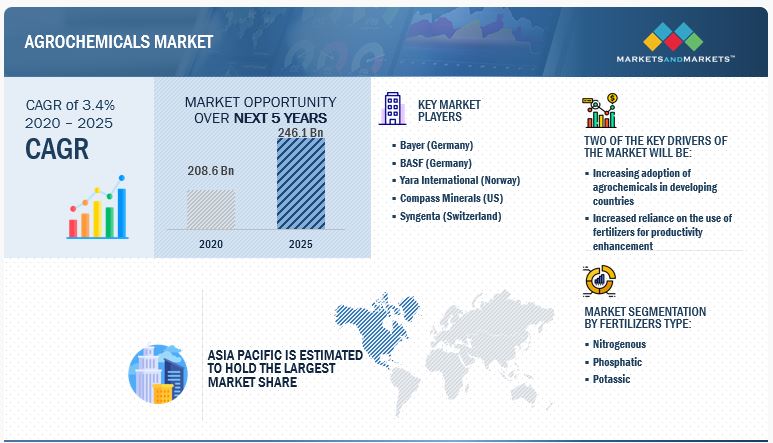

The global agrochemicals market size is predicted to reach USD 246.1 billion by 2025 and is anticipated to expand at a compound annual growth rate (CAGR) of 3.4% from 2020 to 2025. Asia Pacific is estimated to hold the largest market share during the forecast period. The global agrochemicals market size was valued at USD 208.6 billion in 2020.

Nitrogen fertilizer, by fertilizer type, is estimated to account for the largest market share during the forecast period

Nitrogen fertilizers are the most widely used fertilizers in agricultural field. Amongst all nitrogen fertilizer, urea is the most used nitrogenous fertilizer in countries across the globe because of its high N content (46%N). Hence, it is one of the most widely used dry granular sources of nitrogen. It is preferred by the fertilizer manufacturing industry since it is relatively easy to manufacture. On a ton-for-ton basis, urea contains 35% more nitrogen than ammonium nitrate. This has implications on the storage and transport of nitrogen fertilizer products. Urea is considered a relatively stable product to store and transport, and it is for this reason that the transportation of urea is considered very cost-effective in comparison to its most common alternative, ammonium nitrate. Although urea often offers farmers the most nitrogen for the lowest price on the market, special steps must be taken when applying urea to the soil to prevent the loss of nitrogen through a chemical reaction.

Herbicides, by type, is estimated to hold the largest market share during the forecast period

The agrochemicals market, by pesticide type, has been segmented into insecticides, herbicides, fungicides and other. Herbicides accounted for the largest segment during the forecast period. This is attributed to the wide acceptance of herbicides in the cultivation of a variety of crops. They are convenient to use for crops such as sugarcane, rice, soybean, and cotton, among others. Rapidly advancing technology in the agricultural and allied sectors has also impacted conventional agricultural practices. It has made the use of external agents more efficient in terms of productivity. Using herbicides to eradicate weeds at an early stage helps increase the productivity and yield per unit, which has led to increased use by producers across the globe. Rising safety and environmental concerns have led to regulatory action in many countries, causing some restraints for the growth of the herbicides market. Major chemicals such as glyphosate and atrazine, among others, are regularly scrutinized, especially in Europe. However, considering the increasing use of herbicides, the market is very promising and is likely to expand.

Asia Pacific is estimated to hold the largest market share during the forecast period

The Asia Pacific agrochemicals market is fragmented among multinational companies and numerous small-scale manufacturers who produce fertilizers and pesticides depending on the crops cultivated. There are more global players in the market that are trying to enter the Asia Pacific region by undertaking mergers & acquisitions or partnerships. The demand for fertilizers and pesticides has been growing in this region due to the increasing investment of overseas business lines in agricultural inputs to exclusively meet the demand of crop growers for attaining export quality.

Global Agrochemical Companies:

This report includes a study on the marketing and development strategies, along with a study on the product portfolios of the leading companies operating in the agrochemicals market. It consists of the profiles of leading companies such as Bayer (Germany), BASF (Germany), Yara International (Norway), Compass Minerals (US), and Syngenta (Switzerland), Adama Ltd (Israel), Sumitomo Chemicals (Japan), Nufarm Limited (Australia), UPL (India), K+S Group (Germany), and Israel Chemical Company (Israel).

Bayer (Germany) operates through four business segments, namely pharmaceuticals, consumer health, animal health, and crop science. The crop science division of the company has been working on introducing crop protection agrochemical products and digital solutions. The crop protection business offers a broad portfolio of highly effective herbicides, fungicides, insecticides, plant growth regulators, and seed treatment products with chemical or biological modes of action. The company provides extensive customer service to support sustainable agriculture.

Nutrien Ltd (Canada) was formed in 2018 during the merger between Agnum, Inc. (Canada) and Potash Corporation of Saskatchewan Inc. (PotashCrop) (Canada), to become one of the world’s largest premier provider of crops inputs and services. Nutrien has the largest crop nutrient product portfolio, which is combined with an unparalleled global retail distribution network that includes more than 1,500 farm retail centers. The company is a leading manufacturer and distributes over 27 million tons of nitrogen, potash, and phosphate products for industrial, agricultural, and feed customers worldwide. The company has a wide range of agriculture retail network that provides services to over 500,000 grower accounts. It has a network of around 1,700 retail locations in seven countries, along with operations and investments in 14 countries globally. It has its presence North America, South America, Europe, Asia, Africa, and Australia. The company provides its fertilizer products in the dry form and liquid forms. It offers fertilizer products such as nitrogen (dry), nitrogen (liquid), potash(dry), potash (liquid), industrial (dry), and industrial (Liquid).

Related Reports:

Seed Treatment Market by Type, Application Technique (Coating, Dressing, Pelleting), Function (Seed Protection and Seed Enhancement), Formulation, Crop Type (Cereals & Grains, Oilseeds, Fruits & Vegetables) and Region – Global Forecast to 2027

Specialty Fertilizers Market by Technology (Controlled-release Fertilizers, Micronutrients, Water Soluble Fertilizers, and Liquid Fertilizers), Form (Dry and Liquid), Application Method, Type, Crop Type and Region – Global Forecast to 2027

Controlled Release Fertilizer Market by Type (Slow Release, Coated And Encapsulated, Nitrogen Stabilizers), End Use (Agricultural and Non Agricultural), Mode of Application (Foliar, Fertigation, Soil), and Region – Global Forecast to 2026

About MarketsandMarkets™

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines – TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the ’GIVE Growth’ principle, we work with several Forbes Global 2000 B2B companies – helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Media Contact

Company Name: MarketsandMarkets™ Research Private Ltd.

Contact Person: Mr. Aashish Mehra

Email: Send Email

Phone: 18886006441

Address:630 Dundee Road Suite 430

City: Northbrook

State: IL 60062

Country: United States

Website: https://www.marketsandmarkets.com/Market-Reports/global-agro-chemicals-market-report-132.html